The labor market might be entering a "new normal," and...inflation is back

Let’s start with the big hitters.

April’s jobs report came in stronger than expected on Friday, with the U.S. adding 115,000 jobs while unemployment held steady at 4.3%.

This continues a trend that’s defined the 2026 labor market: Consistently under- or overshooting what’s expected of it in ways that make the broader economy increasingly difficult to read cleanly. Economists had forecasted a net gain of ~62,000 for the month, which essentially translates to: “Okay, so not that, then.” Forecasters are always off — it’s like trying to predict the weather down to the atom — but this year’s variance has been a bit comical.

Visual: Axios

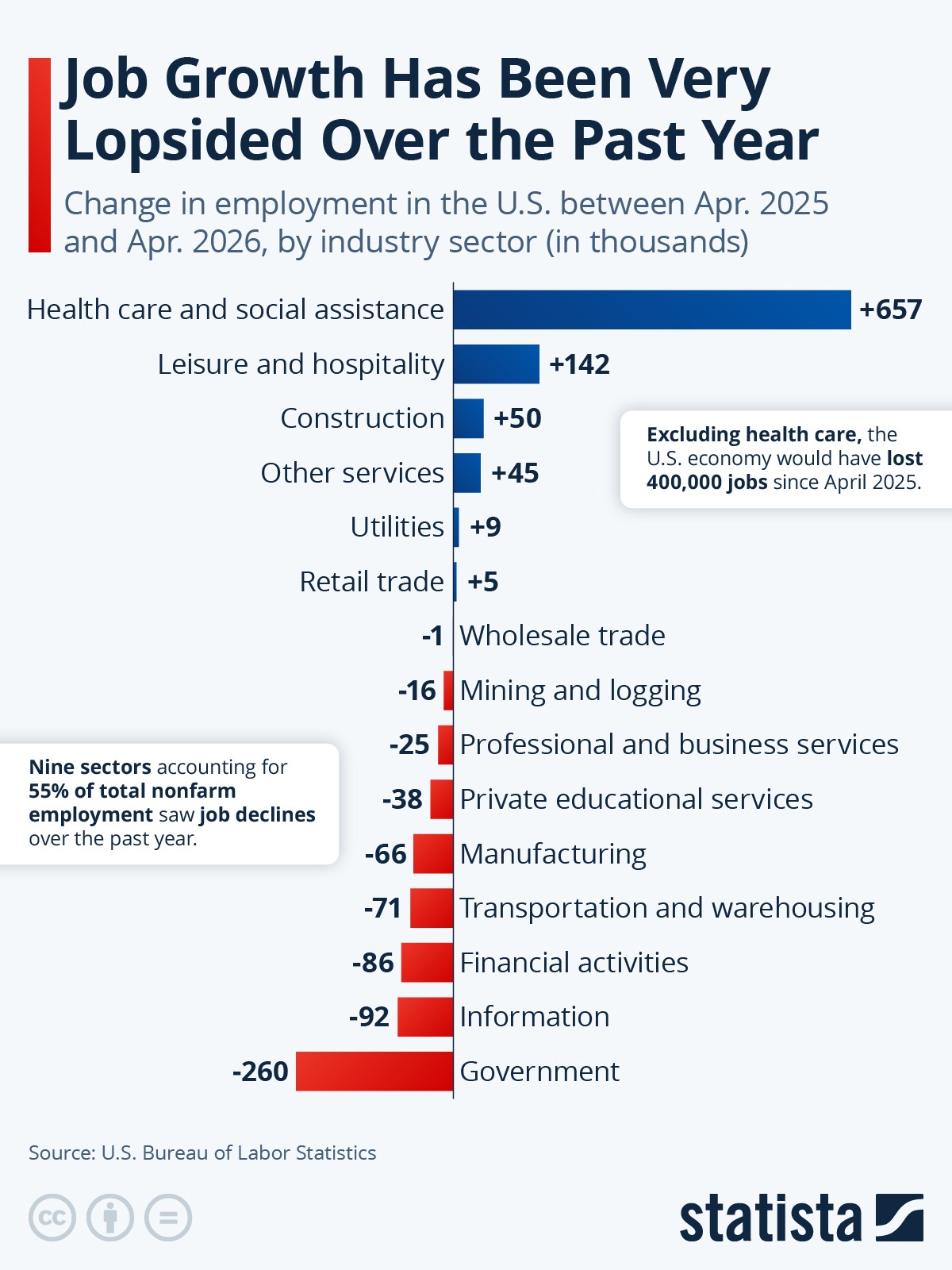

Healthcare, transportation, warehousing, and other service-heavy sectors continued carrying much of the hiring load, helping calm immediate recession fears and pushing markets higher on the idea that the economy remains resilient.

Some intrigue: The “information” sector of the job market shed 13,000 positions in April, continuing a downward trend. This niche has now wiped out over 300,000 jobs since 2022, accounting for 11% of the previous workforce. Elsewhere, the labor force participation rate continued to fall, reaching its lowest level since 2021. This also helps explain why the unemployment rate is so stable despite lower growth: Because the labor force is shrinking.

Visual: Statista

Now, about inflation…

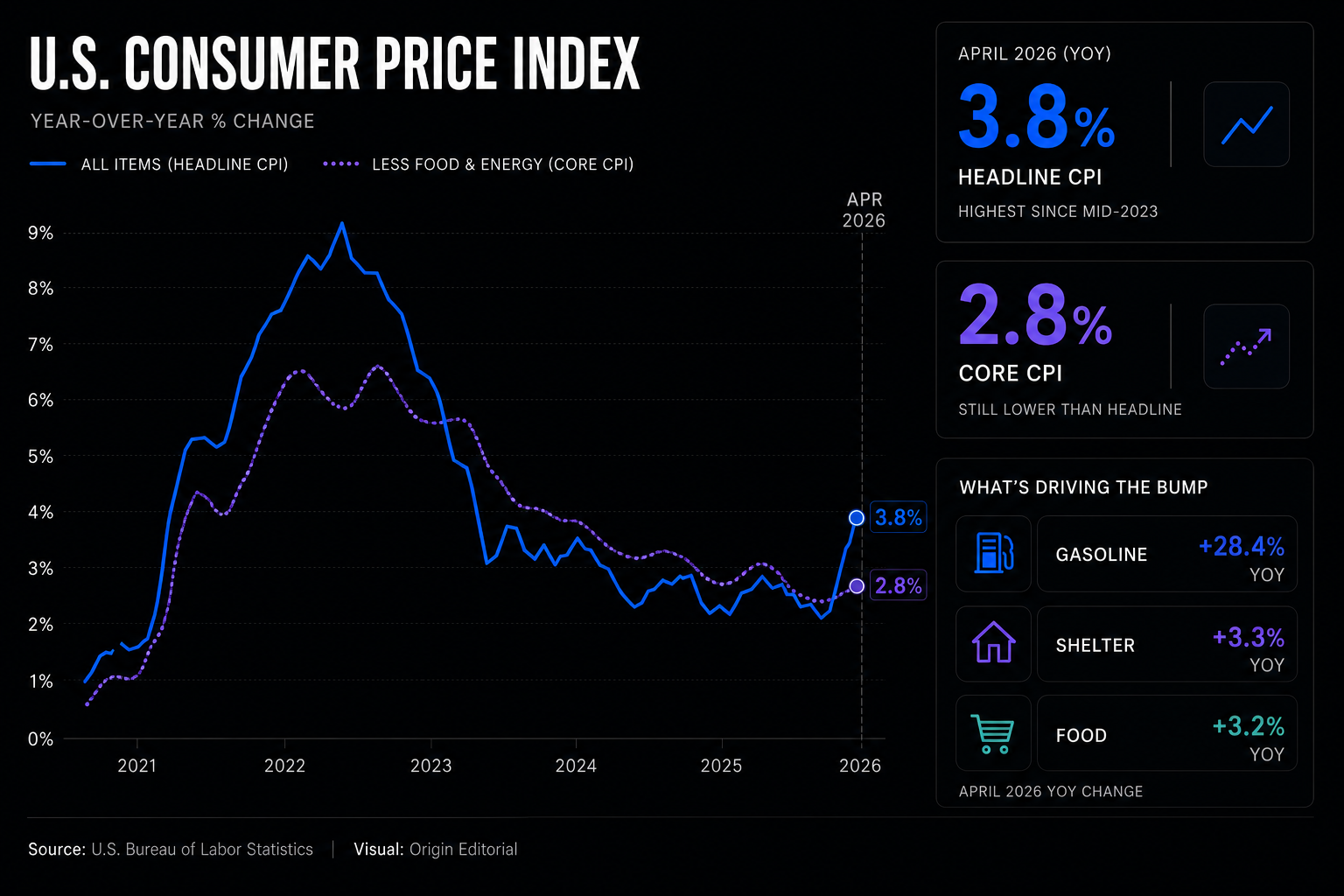

Inflation itself has cooled meaningfully from peak levels, but the spike we saw over the past two months due to energy prices has warped consumer expectations. Today’s report (for April) didn’t help either: Headline CPI rose 3.8% year over year, keeping inflation firmly back in the 3% range for the second straight month, though core inflation — which strips out volatile food and energy costs — came in lower at 2.8%. In other words, the worst of the move is still coming from the exact categories economists like to exclude, and consumers have to actually pay for.

Prior to March’s read, we hadn’t seen a headline inflation number in the 3% range in almost two years — that number being back in the game for two months straight does real damage psychologically. It’s not the 9% from 2022, but it does reaffirm the sort of “inflation PTSD” Americans have developed as a result of it.

Case in point: The New York Fed just reported that one-year inflation expectations rose again to 3.6%, reinforcing the idea that many consumers still expect elevated costs to persist.

And some estimates put real inflation even higher. The personal consumption expenditures index (PCE), which tracks a broader range of expenses than the CPI and is the Fed’s preferred inflation gauge, came in at 3.5% last month — and the non-chained version of the metric, which strips out some of the substitution adjustments used to smooth inflation readings, came in at 5.7%. PCE data lags CPI, so we won’t get another read until the end of the month, but it’s a good reminder for now that inflation is not just a single number or a uniform experience.

Ultimately, this combination of a puzzling job market + rejuvenated inflation puts the Fed in a very paralyzed situation. Not only are they about to usher in a new Chairman — who may or may not want to cut rates — but we’re now dealing with a pocket of: Inflation regression, international conflict, and a labor market that seems to be re-learning who it wants to be. What do you do in that situation? The board of governors will reconvene again on June 16th with their (likely) new leader and two new sets of economic data by then — for now, though, oddsmakers figure about a 95% chance of another hold.

All of this is visible in how consumers feel right now. Consumer sentiment just fell to one of the weakest readings on record. The University of Michigan’s preliminary May sentiment index dropped to 48.2, well below expectations and near historic lows despite relatively stable unemployment and continued consumer spending. That disconnect is perfectly explainable, because ordinary people don’t experience the economy through jobs reports — they experience: Fuel prices, inflation worries, AI-related job fears, expensive housing, and real-life problems.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.