The Fed's inflation alarm just went off again — here's what it means for your wallet

The Federal Reserve's preferred measure of inflation just landed, and the number isn't good — though it could have been worse.

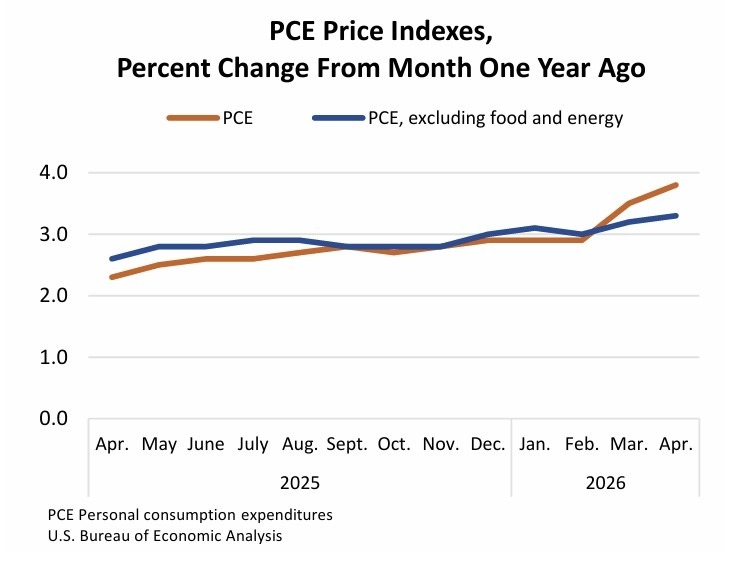

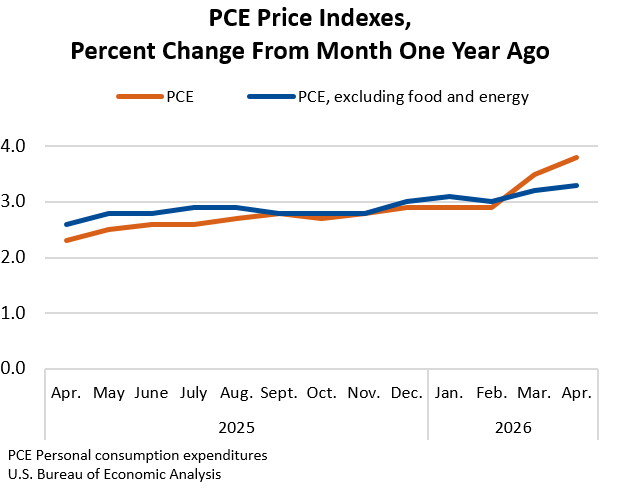

The Personal Consumption Expenditures (PCE) index just came in at 3.8% year-over-year for April, up from 3.5% in March and the highest reading we’ve seen since May 2023. Core PCE, much like our traditional inflation metric, CPI, was notably lower at 3.3%. This is well above the idealistic 2% target Fed officials have been aiming for since 2022, but it wasn’t exactly unexpected — rising oil and gas prices have thwarted inflation data since March, so this is nothing new. The good news (if you want to be optimistic) is that the month-to-month gain came in below expectations at 0.4%, and decelerated from the 0.7% surge we saw in March.

Source: BEA

That deceleration is the one constructive signal in an otherwise uncomfortable report. The energy shock from the war in Iran drove March's ugly monthly number, and April’s data holding in the same upper 3% range suggests it isn't fully passing through to other underlying prices — yet. Whether that holds into May depends almost entirely on what happens with the Strait of Hormuz.

And that’s probably why the stock market didn’t freak out today. Major indices were steady, slightly up, and mostly calm in the face of what would typically be a bearish data point.

Elsewhere, a separate report from the same agency (the BEA is responsible for all of today’s data) revised Q1 GDP growth down to 1.6% annualized, from the initial 2% estimate, reflecting weaker consumer spending and business investment during that period. Historically, that would be a lackluster annual growth rate for the American economy — but this data can vary wildly quarter-to-quarter, so right now, take it with a grain of salt.

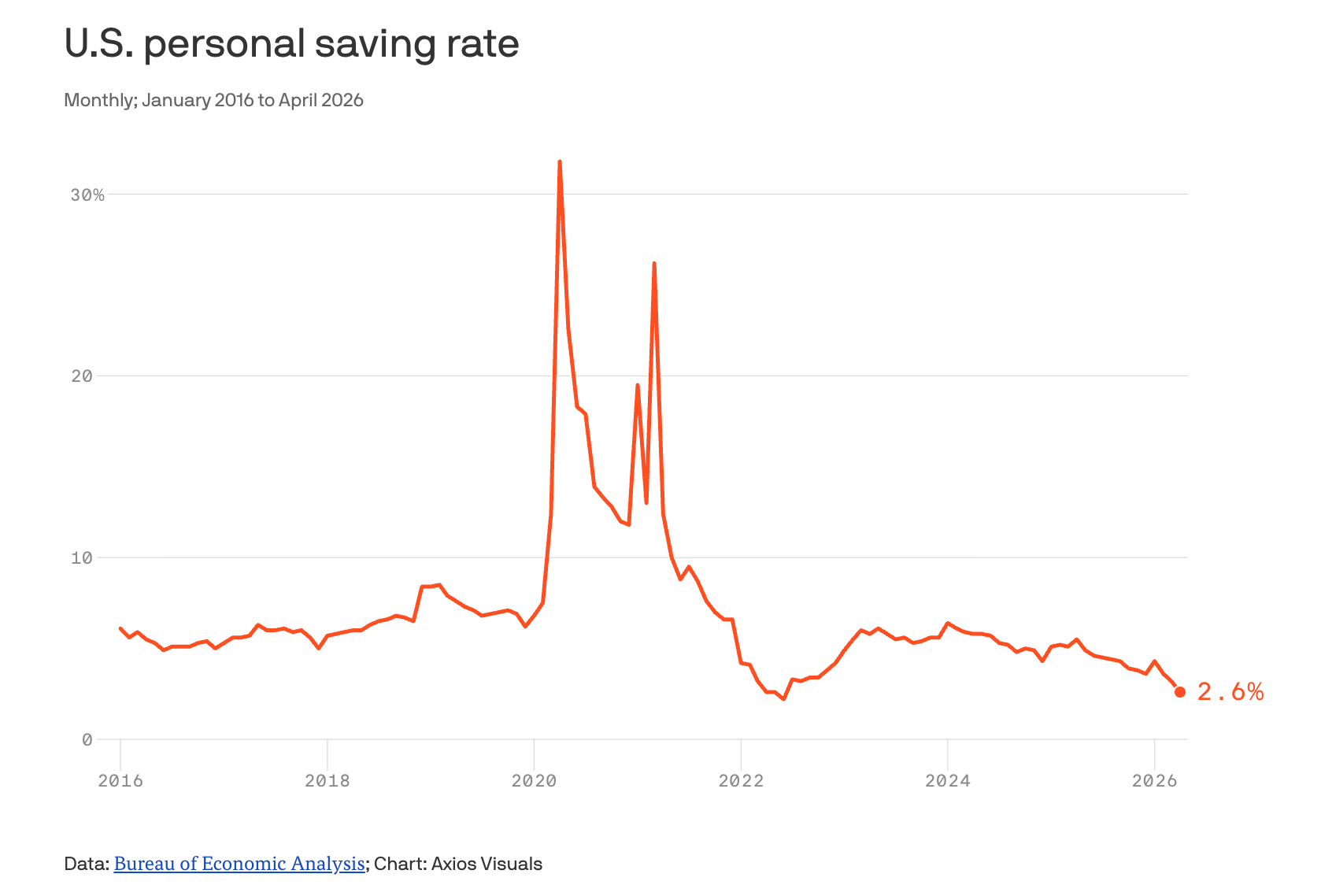

Personal income was also essentially flat in April. Disposable income fell 0.1%, consumer spending rose 0.5%, and most notably, the personal savings rate fell to 2.6%, down a full percentage point from March. Americans spent more while earning less and saving less.

What all of this means for your money comes down to two things: The cost of everyday goods (like fuel) and interest rates. We already understand the inflation half — the cost of living is harsher right now than it was in early Q1. The interest rate side of the equation isn’t that hard to figure out either. Rebounding inflation = higher for longer from the Fed is likely to hold, investors will demand higher bond yields, and subsequently, the cost of borrowing (mortgages especially) will tick up for now.

Also noteworthy here is the Fed’s new Chairman. Kevin Warsh, who just took over as Fed chair, has indicated he believes rates could eventually be lowered — but he's likely to face opposition from the rest of the FOMC. His first meeting is on June 16th, and today's data gives him slightly more breathing room than yesterday's fears suggested — the monthly deceleration on core is real, but not enough to change the fundamental picture. Oddsmakers currently expect the Fed to stay on hold until at least late 2026, and are pricing the likelihood that the next move is a rate increase rather than a cut.

Private labor market data from ADP this week also adds some texture. ADP's weekly pulse showed private employers adding an average of 35,750 jobs per week in the four weeks ending May 9 — down from 40,750 the prior week. Hiring is recovering from the war-driven shock of late February, but it hasn't returned to the pace needed to generate real wage pressure against 3.8% inflation.

Long story short: Inflation above target, growth is slowing (for now), wages are flat, spending is funded by a savings drawdown, 24.5% APR credit cards, and 6.6% mortgage rates are back. Ultimately, Warsh inherits a committee that wants to hike, a president who wants to cut, and data that doesn't cleanly support either.

The Iran deal, if it closes, remains the clearest path out. Reopening the Strait of Hormuz would pull energy prices down, ease headline PCE, and give the Fed cover to at least stop talking about hikes. But JPMorgan still expects oil to average $97 a barrel through year-end, even with a deal.

Until something structurally changes — the Strait reopens, wages accelerate, or the Fed moves — the consumer stays exactly where they've been: spending more, earning less, and running out of cushion.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.

{kind=link}