Tax Brackets For 2026 Are Here

You were supposed to be getting an inflation update in your inbox today — change of plans. Thanks to the government shutdown, the Bureau of Labor Statistics (BLS) has delayed its official release until October 24th, so…we’ll still get that official September inflation data, just a bit belated.

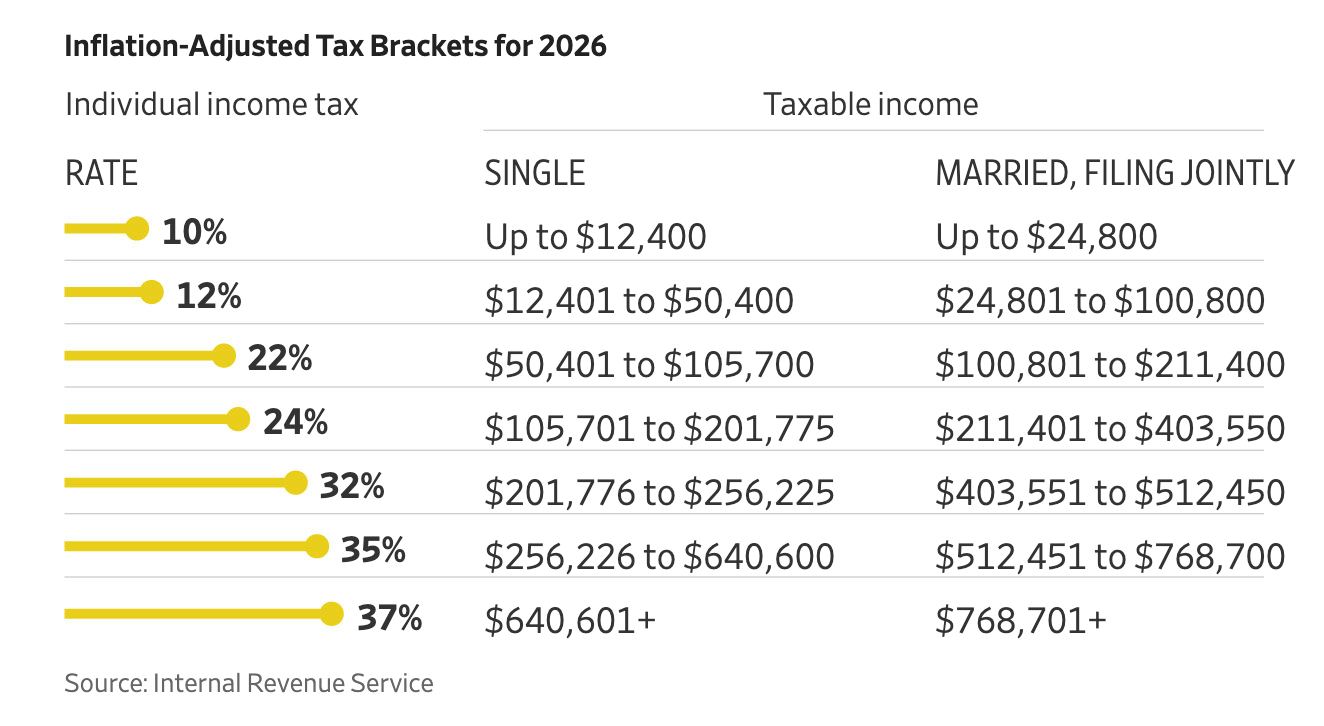

In its stead, we’ve got a tax-related update for you. Every year in October, the IRS unveils its revised tax brackets + rates, and last week, the 2026 edition rolled out. Despite the absence of its expected report, inflation is still doing taxpayers its annual favor. The adjustments are tied to it, after all, and move up accordingly, meaning you’ll be able to earn more before the next slice of your paycheck gets taxed at a higher rate.

With a 4% bump for the lowest brackets and 2.3% for higher ones, filers get a slightly bigger adjustment than last year. For individuals, the 37% top rate now kicks in at $640,600; for couples filing jointly, it’s $768,700, about $17,000 higher than before.

Source: WSJ

The standard deduction is also inching up — $16,100 for single filers and $32,200 for joint filers — so most Americans will owe a bit less overall, maybe a few hundred bucks depending on income. The 0% capital-gains rate will now apply up to $49,450 for singles and $98,900 for couples. The estate tax exclusion is where the real money moves: it’s jumping to $15 million, up from $13.99 million — thanks in part to the Trump administration’s 2025 “Big Beautiful Bill,” which extended and expanded key provisions of the 2017 tax cuts. That tweak alone preserves a six-figure break for the wealthiest households.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.