Inflation hits a three-year high, but the fine print is more interesting

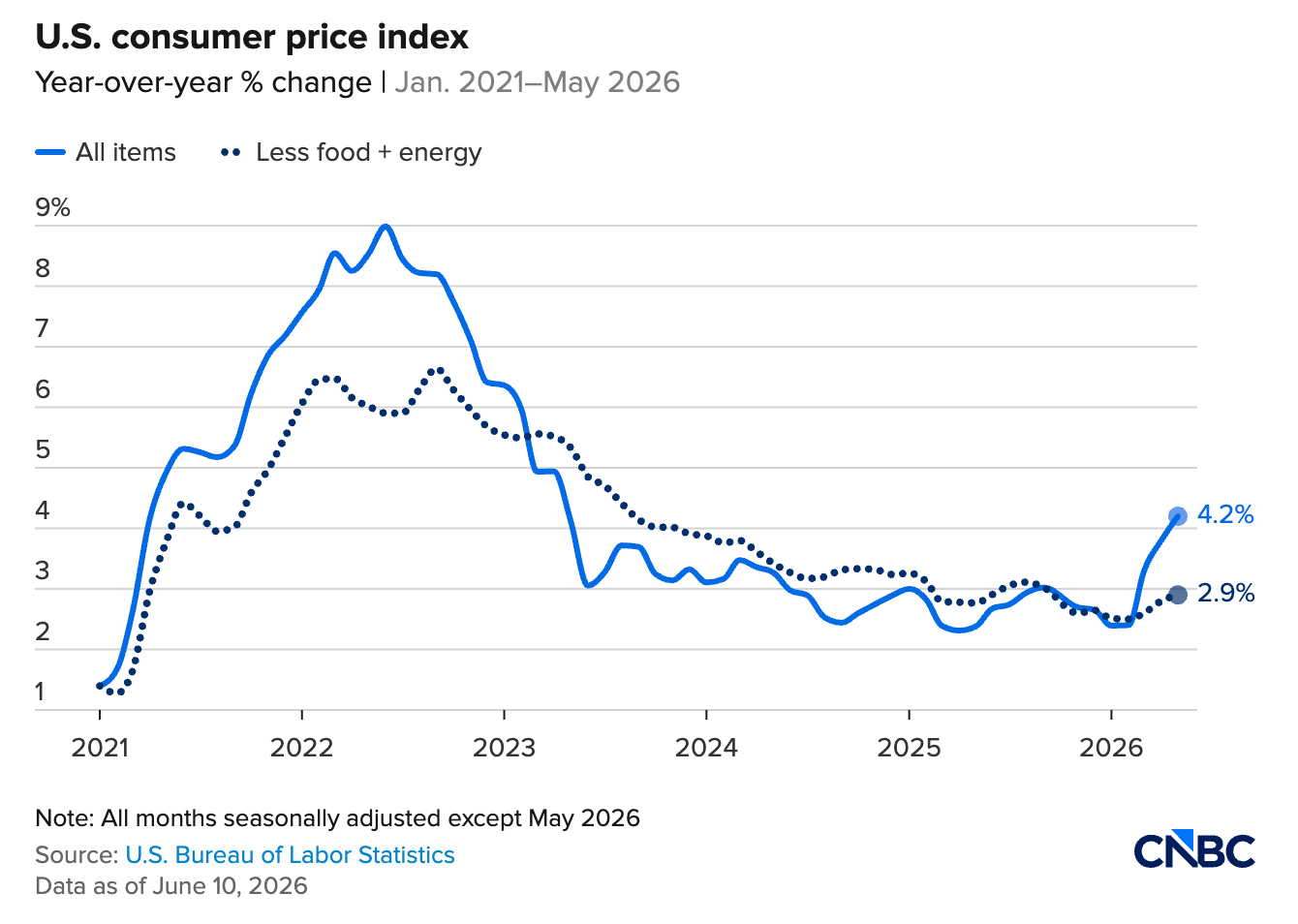

The May CPI report landed Yesterday morning, and unfortunately, it was perfectly aligned with expectations. Most forecasts clustered right around the 4.2% mark, and sure enough, year-over-year inflation came in at exactly that. This is another uptick from the 3.8% we saw in April, the highest reading in over three years, and noticeably higher than the mid-2 % range we had been living in for the past year. Three years of disinflation progress, officially round-tripped.

Just like last month’s report, the composition of the increase matters a lot here. The vast majority of it can be attributed to energy prices — specifically fuel/oil and gasoline — which drove over 60% of the monthly gain. Core inflation (which strips out those volatile categories of food and energy) pretty much substantiates that: It came in at 2.9%, actually rising a bit less (0.2%) month-over-month than the 0.3% economists had expected.

The 12-month energy index now sits at +23.5%, which is what happens when a war chokes the strait that carries a fifth of the world's oil.

Elsewhere, core commodities prices actually fell 0.1% last month, so the tariff-driven goods inflation everyone spent a year bracing for is, at least right now, nowhere to be found. Strip out the war, and underlying inflation is more or less behaving. That's both the reassuring read and the unsettling one — because it means the entire inflation picture currently hinges on a conflict that has broken or threatened its own ceasefire five times in six weeks, most recently yesterday, when Trump warned Iran would "pay the price" for not taking a peace deal. The market's inflation outlook is, functionally, a geopolitics bet.

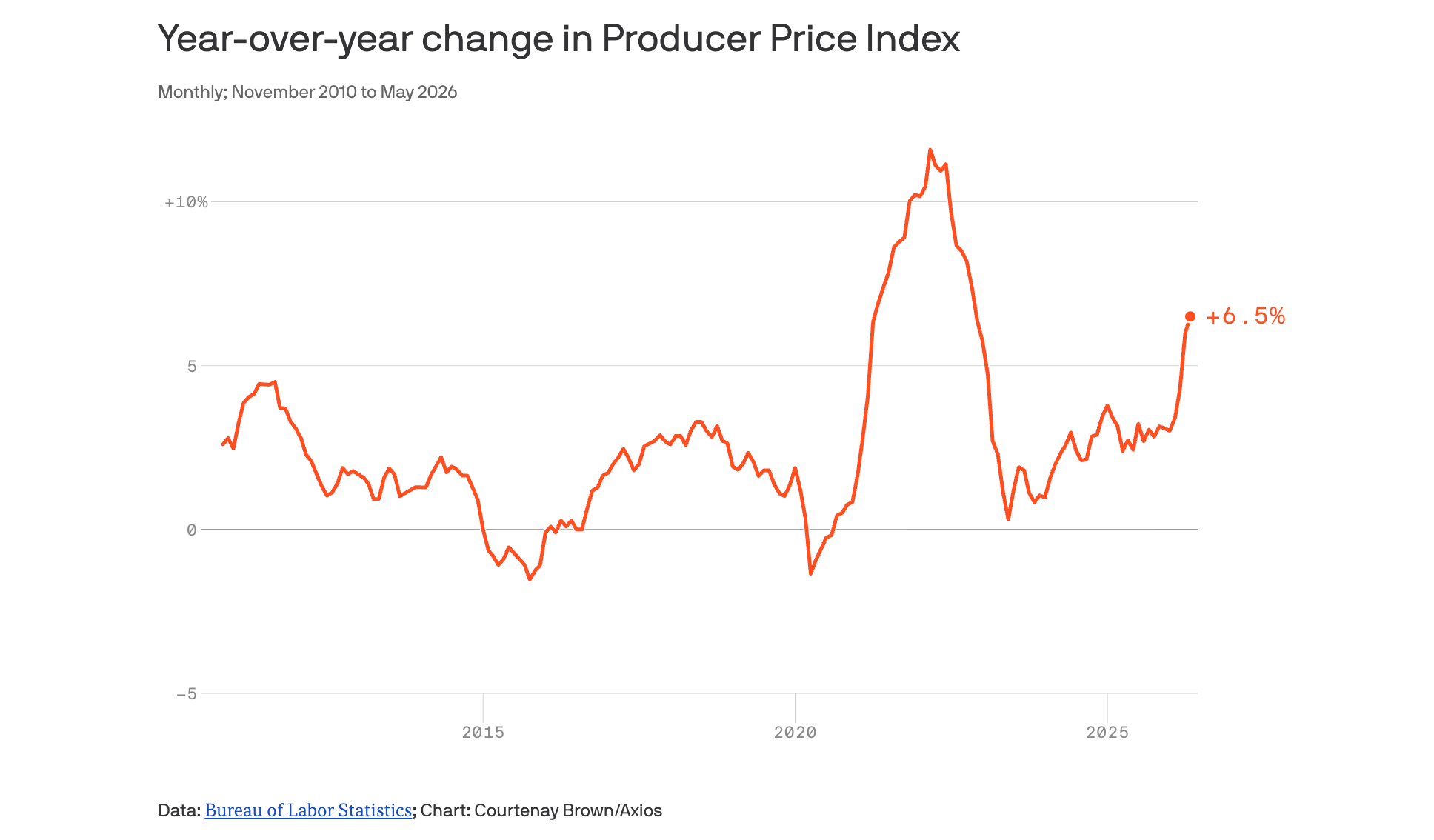

And that conflict-induced price pressure was emphasized even more so in today's Producer Price Index (PPI) report, which measures the prices businesses receive for their goods and services before they ever reach a store shelf — essentially, a preview of where consumer prices are headed next. Wholesale prices rose 1.1% in May, well above the 0.7% economists expected, marking the largest back-to-back monthly increase since 2022 and pushing the annual rate to 6.5% — the hottest since November 2022.

The breakdown makes it almost too easy to identify the culprit: Nearly 80% of May's increase came from goods (physical products like energy, food, and manufactured items, as opposed to services), which rose 2.8% on the month, the largest increase since this series began in 2009. If yesterday's CPI was the "the war hasn't bled into everything else yet" report, today's PPI is the "but it's about to" report. Producers are now absorbing input costs that are rising at more than half the pace at which consumers are currently paying, and that gap only closes through thinner margins or by passing it on to the consumer. The latter of which is eventually inevitable, evidenced by the fact that nearly a third of small businesses are already planning to raise prices.

And all of this comes full circle back to interest rates. The European Central Bank just raised its key rate a quarter point to 2.25%, becoming the first major central bank to act on the same Iran-driven inflation shock the U.S. is grappling with. (But — if it’s any consolation, the ECB’s rates are already over a full percentage point below ours anyway)

That's the backdrop Kevin Warsh inherits as he chairs his first FOMC meeting next week, with the decision landing June 17. We went into the year assuming more rate cuts might be delivered within Q2, and arrived here with zero expected cuts for the rest of 2026. This week's reports didn't make his debut any easier. For now, prognosticators have mostly given up hope. Two of his own voting members — Waller and Hammack — have already publicly floated rate hikes, and per CME FedWatch, futures traders now expect zero rate cuts in all of 2026, which aligns with many economists' projections.

So, ultimately, the "inflation is mostly energy" framing is analytically true and emotionally useless — energy inflation is still inflation, and it’s putting upward pressure on interest rates for now. And in the lived experience, nobody actually experiences the granularities of a CPI report in their day-to-day transactions; they just experience: Ouch. If the Strait reopens, this all unwinds relatively quickly — energy base effects reverse, the headline falls back toward the core, and Warsh gets the breathing room every new Fed chair wants.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.