Homes are still extremely unaffordable for most Americans

Housing affordability "improved" for roughly seven straight months through April of this year, but then mortgage rates jumped in May, and we're basically back where we started. This is the housing crisis in miniature: A few basis points move, and the whole narrative switches again.

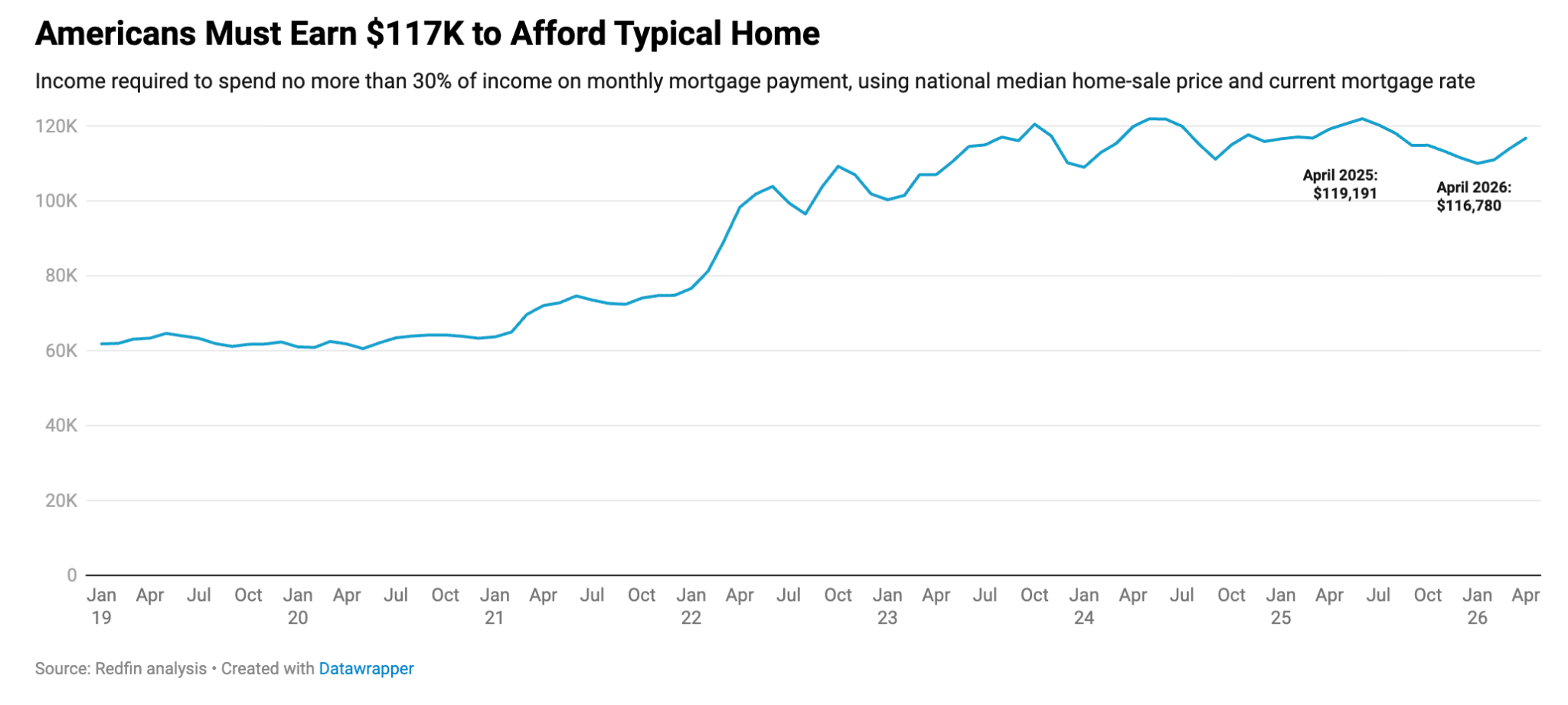

You’ll need to earn roughly $117,000 to afford the median home in America, but the typical U.S. household (not individual) earns roughly $88,000. That's a $29,000 gap, or 32% above average. If we’re being candid — even pretending that's "improving" because it shrank from $31,000 last year is…a bit of a cope. It's like calling a sinking ship "stable" because the leak slowed.

Source: Redfin

But how can mortgage rates do that much damage? Here's the mechanics: Rates dropped from roughly 6.73% in April 2025 down to 6.33% in April 2026, and incomes rose by about 4% year-over-year, so homes became slightly less unaffordable. Not affordable, just slightly less worse. The income needed to afford a typical home is still below its peak ($119,000), but a regression from its previous low of $110,000, for sure. As a result, the median American homebuyer would need to spend about 40% of their income on housing to buy a typical home, and that is…also pre-tax. The proportion of actual net income that the mortgage would consume is actually illegal. Seriously, like a lender will genuinely not allow it — the general rule of thumb is 30% of your gross monthly income, and we’re already way past that.

And there’s a rip current: If you do own a home, the real value of it is eroding. Since June 2025, inflation has outpaced home price appreciation. Nominal prices are up 1.7% year-over-year, but inflation is eating into the purchasing power of that increase. For over a decade, homeownership was wealth-building, and presently it’s just treading water. So…no one really wins. Homeowners get less appreciation, and most prospective buyers are still priced out, which creates a very tight tug-of-war between buyers and owners.

Interestingly, investors are simultaneously backing off, too. U.S. investor home purchases fell 6% year-over-year in the first quarter to their lowest level since 2020. That's actually good news for first-time buyers — fewer institutional investors bidding up entry-level properties. But why they're backing off is the warning. Elevated housing costs squeezed potential returns. The median capital gain for a home sold by an investor was $196,618 in Q1, up 5.3% year-over-year, but that pales in comparison to the double-digit gains common in 2020 and 2021.

So, the overall narrative reads: Affordability improved because rates dipped for seven months, then rates jumped and erased it. The structural problem — you need six figures for a normal home, the typical household makes $88K — hasn't moved. Real home values are eroding. Investor returns disappeared. Most major metros are still brutal.

This is a brief respite, not recovery.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.