Everyone is confused, and inflation is loitering

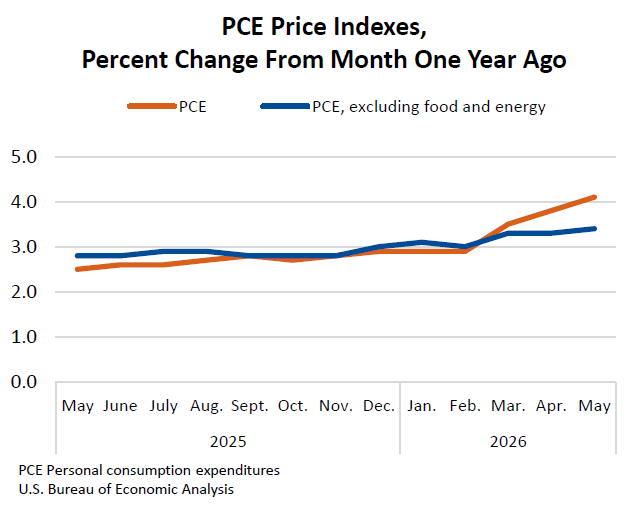

The title pretty much sums it up. CPI usually gets most of the headlines, but the underrated Personal Consumption Expenditures (PCE) price index — a proxy for the Fed’s preferred measure of inflation — dropped today, and it was, well, yeah, high, coming in at 4.1%, which is the highest we’ve seen since April 2023. At the core of it (literally), what the Fed actually wants to see is Core PCE, and that too came in hot at 3.4%, the highest since October of 2023 and up 0.3% from April’s reading.

But that wasn’t exactly unexpected; it was pretty much right in line with expectations, and, per usual this year, it can largely be chalked up to higher energy (specifically fuel and oil) prices over the past few months. Oil prices have fallen precipitously in recent weeks due to the prospect of a deal with Iran — but this is May’s data — that easing will take a while to come through in the data.

So, is this “bad” news? Yes, in the sense that it’s higher than the standard 2% long-term inflation target, and no in the sense that it was: Expected, explicable, and potentially transitory.

Source: BEA

Some other positive data that came out of this report: The Personal Savings Rate, which recently hit its lowest level (2.6%) since 2022, ticked back up a bit to 3%. The data dump also included the BEA’s third estimate of Q1 GDP growth, which was revised upward to 2.1%, up 0.5% from last month’s projection.

That’s a silver lining for sure, but overall, this data pretty much leaves the Federal Reserve exactly where it has been — stuck. Until this conflict-derived inflation spike sorts itself out, rate cuts are out of the question, and rate hikes are actually in play again. Bank of America recently became the most hawkish prophet of the bunch, projecting potentially three rate hikes before the end of 2026 — they pay almost nothing in terms of interest on your savings anyway, so they don’t have to worry about rate hikes increasing their liabilities. Other bettors are a bit more dovish, with most oddsmakers expecting another hold at the Fed’s next meeting in late July. The rest of the year is…yeah, up in the air.

All of this data culminates in, essentially: Confirmation of nothing unexpected, which was not good enough for investors to allow a purely green trading session today. Why? Other factors. The AI bubble narrative has regained some traction this week, sending stocks (especially tech) spiraling on multiple trading days so far.

Then, yesterday after the close, newly minted AI giant Micron reported earnings: $41.46 billion in revenue, up 74% sequentially and 346% year over year. Adjusted earnings of $25.11 per share beat Wall Street's $20.49 estimate by 22%. Gross margin hit 84.9% — a company record. Free cash flow hit $18.3 billion — another record. Data center revenue reached $25 billion in the quarter alone. The company guided for Q4 revenue of $50 billion and EPS of $31. Shares rose nearly 15% after hours.

That alone sent both the stock and Nasdaq Futures soaring after hours, and then back down to earth today. Investors basically said: Wow…nice, but also: We didn’t forget. $MU and a few other AI names were able to maintain their spike through today, but the tech sector as a whole ultimately treaded water at best.

Apple also just announced that they’re raising prices by up to 25% on certain MacBook and iPad devices. Genuinely comedic timing to drop this right after an inflation report, and so it’s understandable that this would bleed over into inflation + rate hike fears as well.

It’s already been a choppy week, and that’s on top of a choppy year — stocks have been unable to find directional conviction for months now due to various reasons. Oscillating between narratives like AI being either a bubble or the new industrial revolution, dealing with geopolitical turmoil, and now dealing with inflation. We have record leverage, record uncertainty, and record innovation — all at once.

The internal confliction that’s manifested as volatility is ultimately justified.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.