Defining an AI bubble

Revolutionary innovations often have one thing in common: They sometimes create a stock market bubble. That sounds ironic, because you’d think that if something were truly revolutionary, the “bubble” would actually be justified, and therefore not one — not the case.

Take the internet, for example; it’s changed the world forever, has it not? Undeniably, yes, and yet…the dot-com bubble still happened. We observe a similar pattern in other supercycle-type eras of history, such as the Electrification Boom, the railway breakthrough, and Canal Mania; the list could expand.

Is AI the exception?

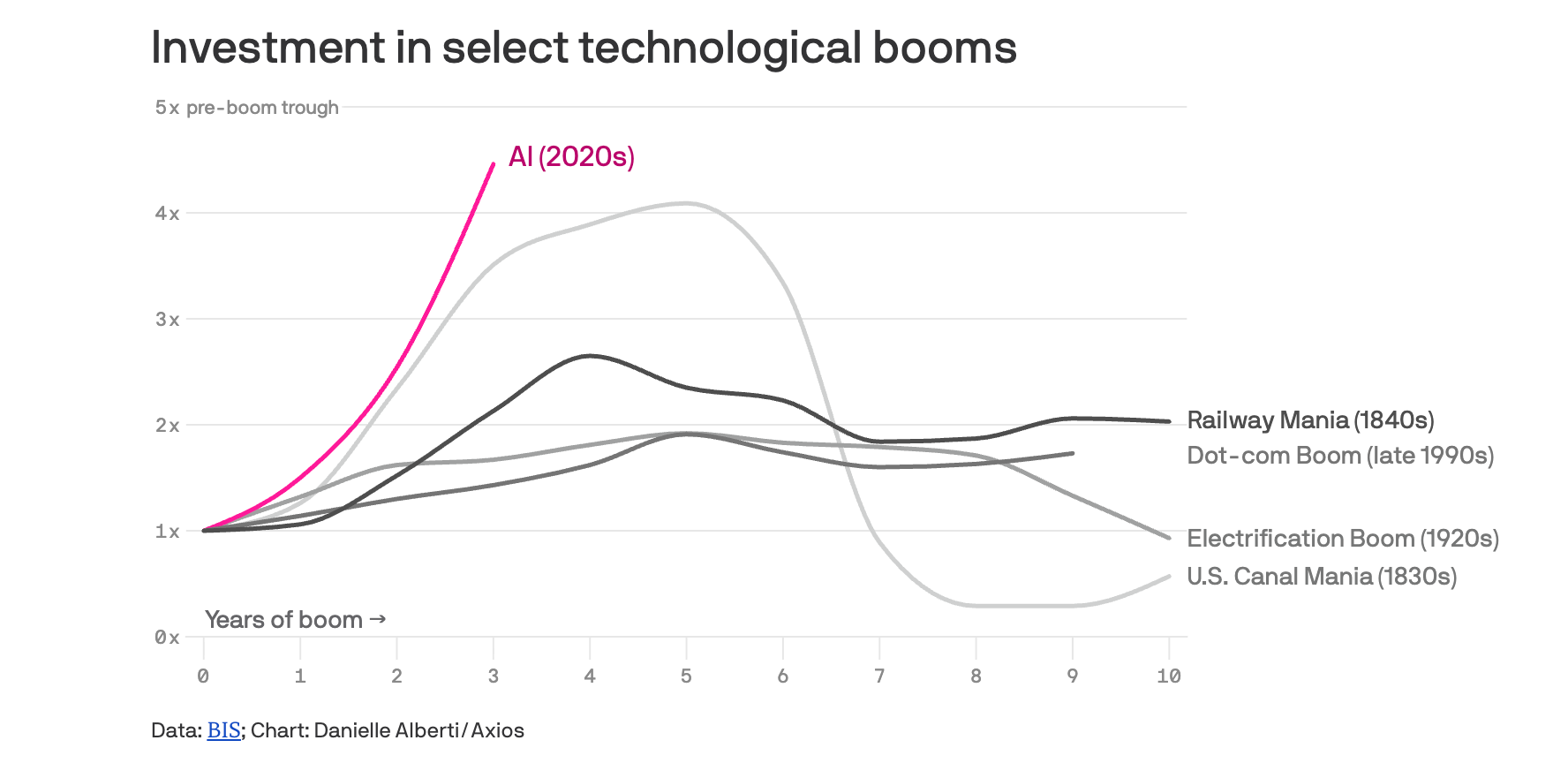

The Bank for International Settlements — literally the central bank for central banks — says probably not. In a recent report, the BIS mapped AI investment against Railway Mania, the Electrification Boom, and the dot-com bubble, and found the current buildout rising faster and steeper than all of them in its first few years. The BIS's own words: These historical episodes "ended with an eventual reversal in investment, inducing economy-wide recessions." Their read on AI: "scale and pace" bearing "resemblance to these precedents."

Ok, so — bubble, decided, we can all go home. Except not really, because the case for this time being different is also loaded with real numbers, not just vibes.

The bull case

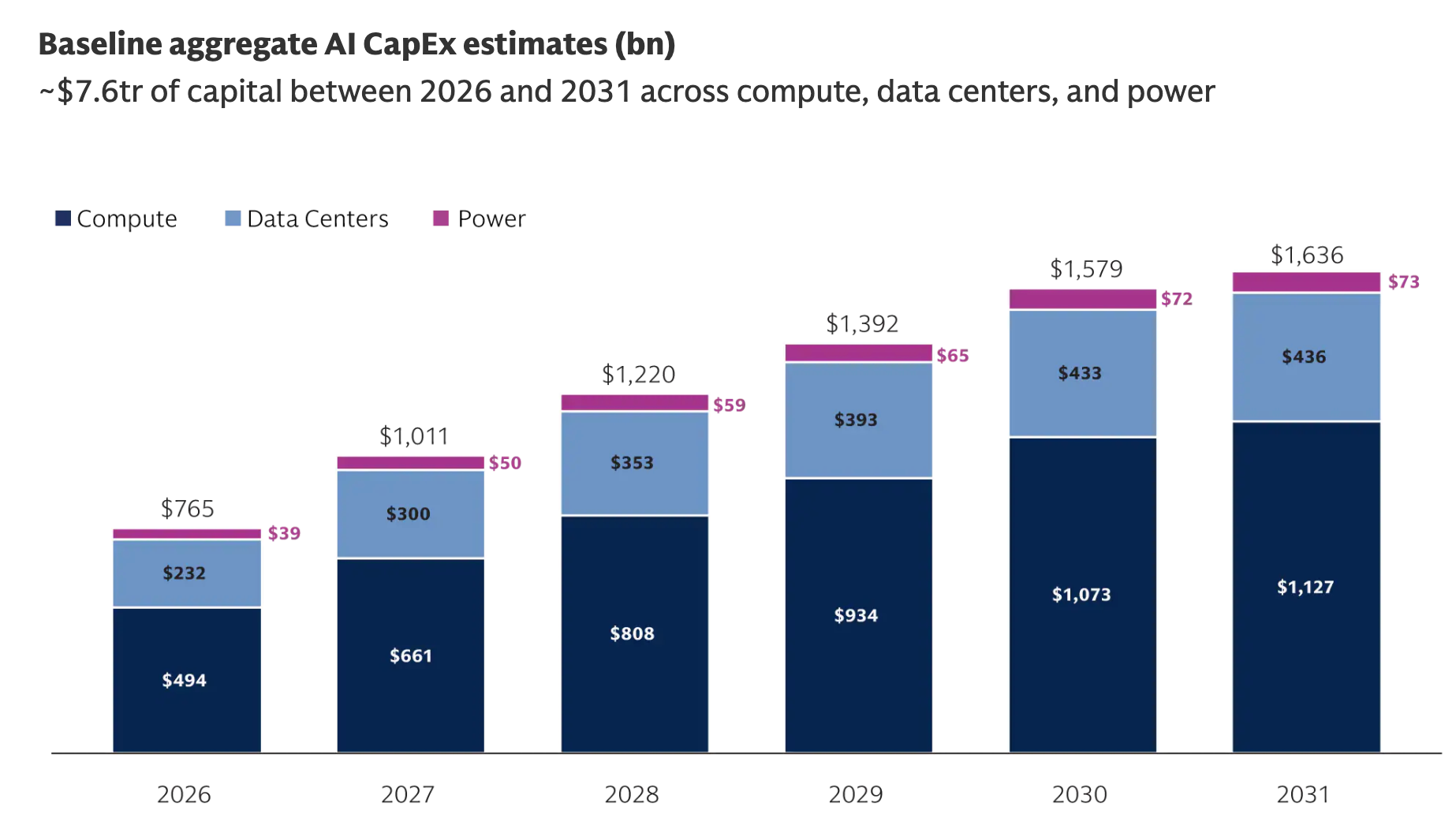

The AI buildout is different in what the money buys: Dot-com capital went to marketing and sales subsidies; AI capital buys GPU clusters, data centers, and power contracts — physical infrastructure with 15-to-20-year return horizons, the kind of capex ratio you'd expect from a utility. Meta's capex is now tracking at 54% of sales, Microsoft's at 47%, and Alphabet's at 46%. Goldman Sachs' own baseline model, anchored to Wall Street's forward estimates for Nvidia's data-center revenue, projects $765 billion in annual AI capex for 2026, climbing to $1.6 trillion by 2031 — roughly $7.6 trillion cumulative over that stretch. That's a full-on, industrial-style buildout with a multi-year runway already priced in by the people actually writing the checks.

Source: Goldman Sachs

Again, watching the money. Not only are companies investing in AI expenditures, but venture capital is funding startups focused on it. AI companies absorbed nearly 80% of global VC in Q1 2026 — $240 billion of $297 billion in a single quarter. The capital is chasing compute — GPU procurement, data center commitments, and energy contracts at a scale that "rivals national grid projects," as one analysis put it. Nvidia alone recorded $75.2 billion in quarterly data-center revenue, which is about as concrete as evidence gets that this money is buying physical infrastructure, not vibes.

Retail is piling in. Now, yes, this is often read as “dumb money at the top,” but here it's also a real demand signal. Retail investors have bought $22.5 billion in U.S.-listed semiconductor ETFs year-to-date, a figure that has surged over 1,000% since early April. As of June, individual investors were also spending $1.9 billion a day on semiconductor options, up 16% from May's record. Whatever you think of retail timing, that's real capital voting with real dollars that the chip demand is durable.

The big names: Anthropic hit $30 billion in annualized revenue by April on 1,400% year-over-year growth. That's real revenue and actual paying customers — today. OpenAI, the other AI giant, generates billions in subscription and API revenue. Anecdotes like these lie in stark contrast to something like the dot-com bubble in 1999 when internet companies were burning cash on customer acquisition with no real business models attached.

The bear case

Concentration risk sits atop this pile. The IT sector now makes up 39% of the S&P 500's total market cap — above the dot-com peak of ~33%. Include Amazon and Netflix in that bucket and tech is half the entire index, compared to 29% at the dot-com top. The Shiller P/E10 — the valuation gauge that smooths out short-term earnings noise — sits at almost 42, a level this market has only touched once before in 140-plus years: right before the dot-com crash.

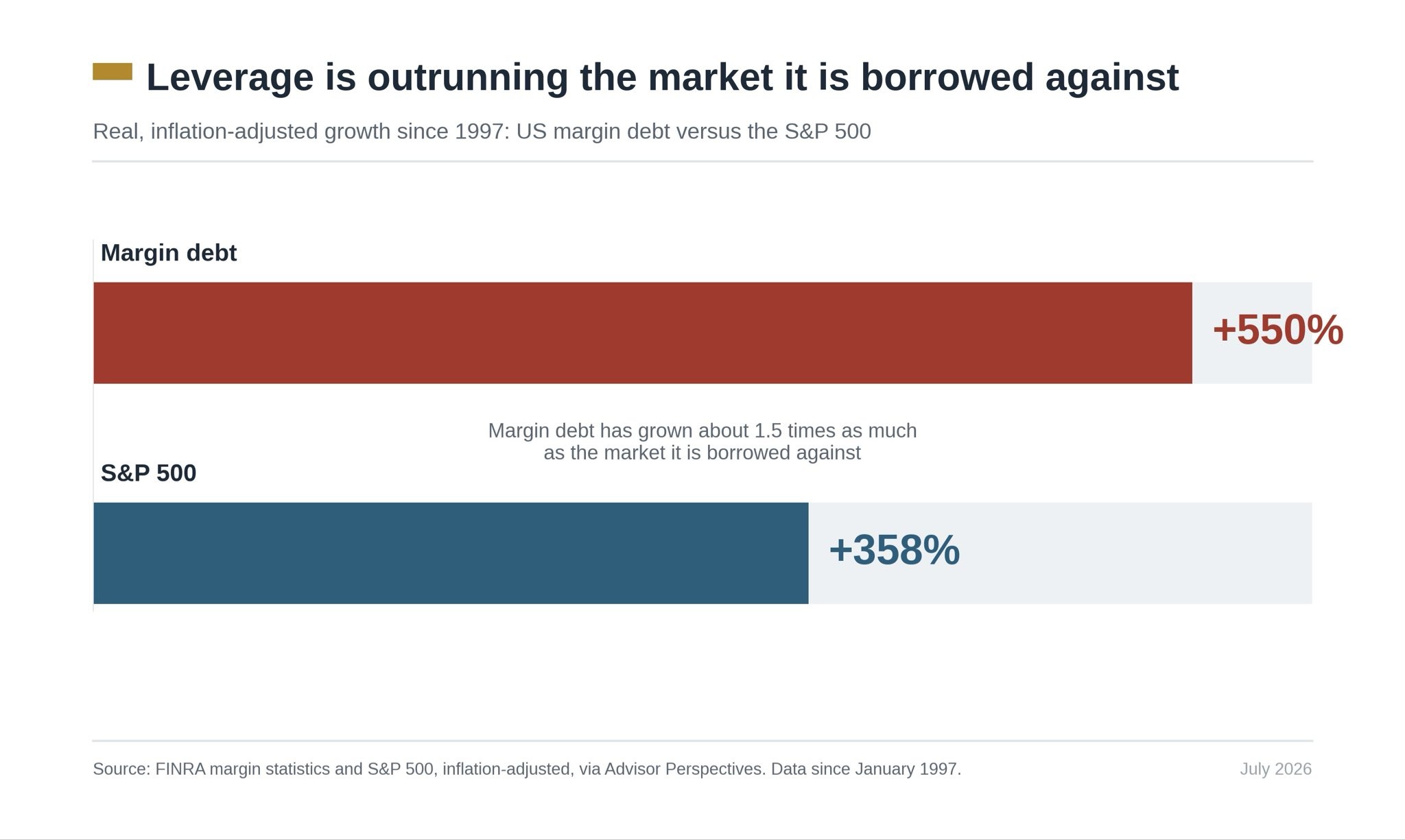

A lot of this cycle is funded by historic leverage, too. Margin debt just hit a record $1.42 trillion, up 53.7% year over year. Worth knowing: margin debt has peaked right around every major market top over the last three cycles — March 2000, mid-2007, and late 2021 — each time a few months ahead of the actual crash. It's currently at its all-time high, right alongside the S&P.

Source: FINRA

Then there's the number that should worry you most if you're trying to figure out whether the spending is justified: Sequoia's David Cahn pegs the gap between what hyperscalers are spending on AI infrastructure and what the AI ecosystem is actually generating in revenue at roughly $600 billion a year — and it's widening, not closing. Allianz puts the divergence at 46%, which already tops the 32% gap that preceded the 2001 telecom correction. Infrastructure spend is scaling roughly 50% faster than revenue right now.

The hidden narrative dichotomies

But that gap isn't evenly distributed, and this is the split screen worth understanding: There's a difference between the people selling picks and shovels and the people panning for gold.

Chipmakers like Micron are booking record margins right now because they get paid the moment the infrastructure gets built — their revenue doesn't depend on whether ChatGPT wrappers or AI agents ever turn a profit. They're capturing capex dollars as they're spent, full stop. The exposure sits one layer up, with the foundation-model companies and application-layer startups who have to actually convert that infrastructure into revenue that justifies its cost. If AI monetization stalls out, the shovel-sellers already got paid. The people who bet on gold in the ground are the ones left holding the bag.

And here's another plot twist: The Magnificent Seven — the stocks most associated with the AI trade — are underperforming the market this year. Down 3.1% on average while the S&P is up 8.7%. Microsoft's having its worst month since 2000. Meta's down 11% in June. The money is shifting away from companies spending on AI and toward the companies supplying the picks and shovels — chipmakers like Micron and Broadcom. UBS called it "increasing shareholder pressure to justify AI spending."

Putting it all together

So: Is this a bubble? The valuation multiples say yes, the concentration risk nods, and the margin debt raw data says maybe. But the actual revenue at the top of the food chain — the Anthropic and OpenAI growth curves — says this might be the rare boom with real fundamentals underneath the froth.

Historically, both things have been true at the same time right before the correction. The railroads got built. The fiber got laid. The bubbles still popped.

Whether AI escapes that pattern probably depends on whether the $600 billion revenue gap closes before the capital markets lose patience waiting for it to.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.