Market Volatility is Stressful — But It Didn't Come Out of Nowhere

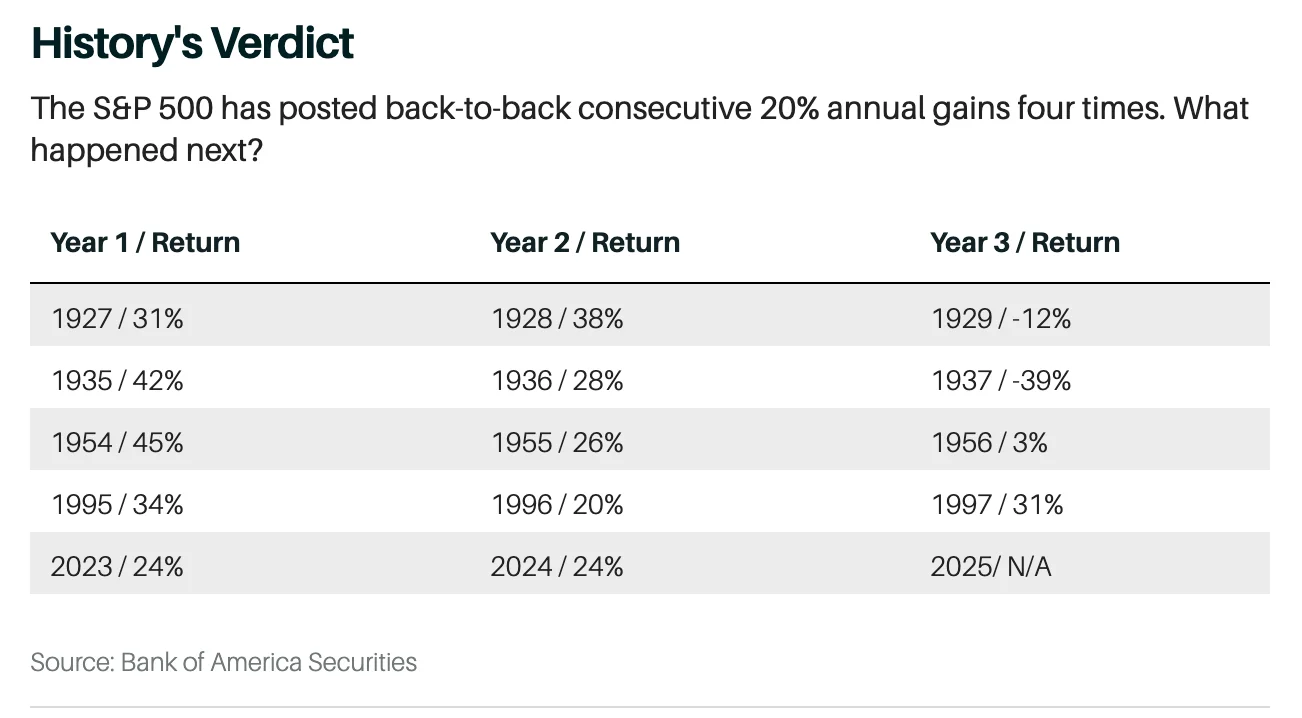

Save for the brief correction that markets experienced in 2022, investors have enjoyed nothing short of market euphoria over the last few years. Between the pandemic flash crash in March 2020 and its all-time high in February 2025, the S&P 500 posted cumulative gains of 141% — that’s an average annual return of 28.2%, an unprecedented pace, and localized gains in sectors like AI and tech have far exceeded even that. So observers knew going into this year that markets would likely cool off a bit: Before 2024, the S&P 500 had only put up back-to-back years of 20%+ returns four times in history. A bear market followed in two cases; a meager 3% gain followed the third; and a continued rally had happened only once, in 1997.

So the drawdown we’ve seen this year was in the cards. The open questions were what would catalyze it, and just how bad would it get?

Source: Barron’s

For the first six weeks of the year, markets eked out modest gains, but sentiment quickly soured as the new presidential administration began talking up its tariff plans. Though tariffs are always controversial due to their inherently politically charged and economically complex nature, markets primarily focus on one thing: the inflationary pressure and geopolitical turbulence tariffs might trigger.

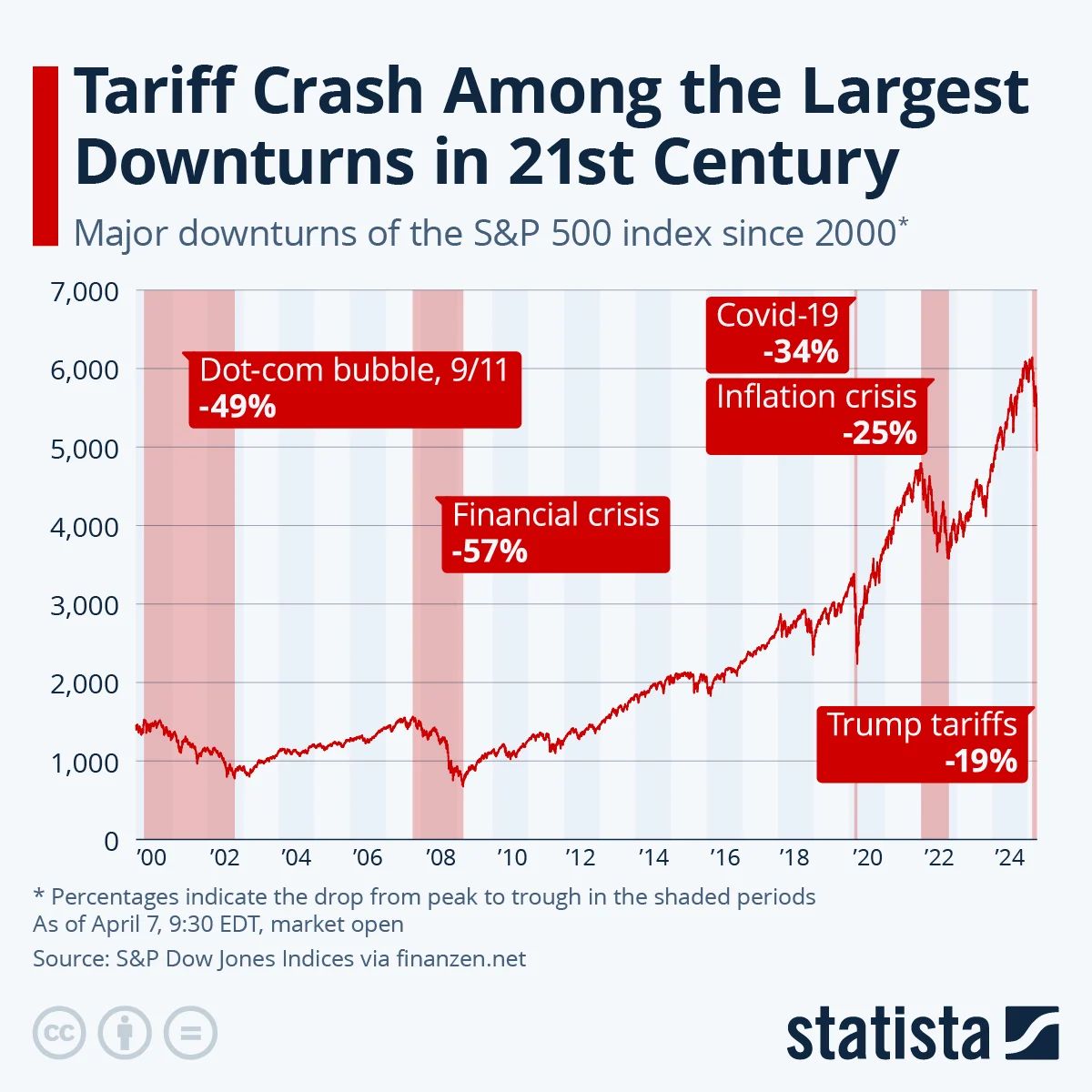

In many ways, that fear becomes self-fulfilling. Investors expected a selloff when new tariffs were announced, and so they sold. After Trump announced a slate of sweeping tariffs last week, markets had their worst stretch since the brief pandemic crash, shedding over $6 trillion in just two days. Major indices fell 4% to 5% on back-to-back days, an infrequent event and a clear reminder of how powerful sentiment is in shaping the market. The S&P 500’s tariff-fueled drop has now marked the fourth-worst market drawdown in the 21st century, coming in just behind the 2022 correction. The average effective tariff rate is now projected to jump from 2.5% to 22% in the coming weeks — the highest level since 1910 — adding further fuel to economic uncertainty.

Source: Statista

Even the U.S. dollar, which economic theory suggests should strengthen under tariffs, reacted in the opposite direction. The dollar index dropped after the announcement, not due to import shifts, but because of anxiety — which brings us to the fact that recession anxiety is now swirling. After last week’s tariff announcement, J.P. Morgan was the first major firm to formally project a recession this year, and others followed suit. While inflation remains stubborn, the bigger fear is that tariffs will undercut growth by pressuring consumers and businesses that are already stretched thin. In normal times, the Fed might step in to cushion the blow, but with inflation still sticky, the central bank has little room to maneuver. Rate cuts could reignite price pressures, while holding at the current rate risks increasing pressure in an already expensive lending environment. It’s a lose-lose setup, and markets know it. Economists now warn that inflation could climb back toward 4% by year’s end, a level that might look modest on paper, but could be highly disruptive in this environment.

Following last week’s nosedive, futures for major indices were down significantly in the pre-market on Monday — the Russell 2000 small-cap index touched -7% at one point, while the S&P 500 and Nasdaq dropped about 4% to 5%. But when trading began, there was a quick rebound, reflecting the volatility that bear markets are notorious for. Today (Tuesday), all major indices and large-cap tech stocks opened green and eventually turned back red after digesting the news of the day.

For individual investors, there’s no denying that this is a tough, uncertain situation. But while the broader economy and political landscape are out of our hands, there are still some important things to remember that might bring some comfort (or at least stop you spiraling):

- The average bear market (and we’re not technically in one yet) drops about 36% and lasts 289 days, but bull markets return 114% on average and win out in the long run. Historically, bear markets show up every 3.6 years, meaning you’ll face around 14 of them over a 50-year investing journey. Still, stocks rise roughly 78% of the time overall. Just stay patient, stay objective, and remember: When the market is volatile, it still tallies false breakouts, so don’t be fooled by big green days.

- Sometimes the most difficult thing to do is nothing. Negative experiences can make us feel like we need to make some kind of change, but this isn’t always the case, especially when it comes to investing. If an investor had sold their $SPY, for example (or pivoted to something more risk-averse like bonds) during the 2020 market crash, they would’ve missed out on one of the index’s best years ever in the months to come, followed by another strong gain in 2021.

- If you’re wary of investing right now, consider cash. With volatility back and uncertainty rising, many investors are opting for safety. Over $60 billion flowed into money-market funds in just the first few days of April last week, pushing total assets to a record $7.4 trillion. And with interest rates still relatively elevated — some banks are offering 4% APY or more on high-yield savings — sitting in cash doesn’t feel like sitting out.

This content originally appeared in The Gist, Origin's twice-weekly personal finance newsletter.

Answers to your questions

Yes. Origin offers partner access so you can manage your finances together at no additional cost. You’ll be able to filter transactions by member—making it easy to see which spending is yours and which belongs to your partner.

Yes. You can edit existing transactions and add new ones directly in Origin, so your records stay accurate and personalized.

Origin connects securely through trusted partners including Plaid, MX, and Mastercard.

Yes. Origin supports CSV uploads. You can upload a .csv file of your transactions, and we’ll import them into your account.

Yes. Your data is protected with bank-level security and advanced encryption. When you connect accounts through Origin, your login credentials are never shared with us. Instead, our partners generate secure tokens that let Origin access only the data you authorize—keeping your personal information private while enabling personalized insights.

Yes. You have full control to organize your spending in Origin. Transactions are automatically categorized by Origin, but you can always edit categories, add your own tags, and filter transactions however you like—so your spending reflects the way you actually manage money.